.

Also question is, what is a mixed measurement?

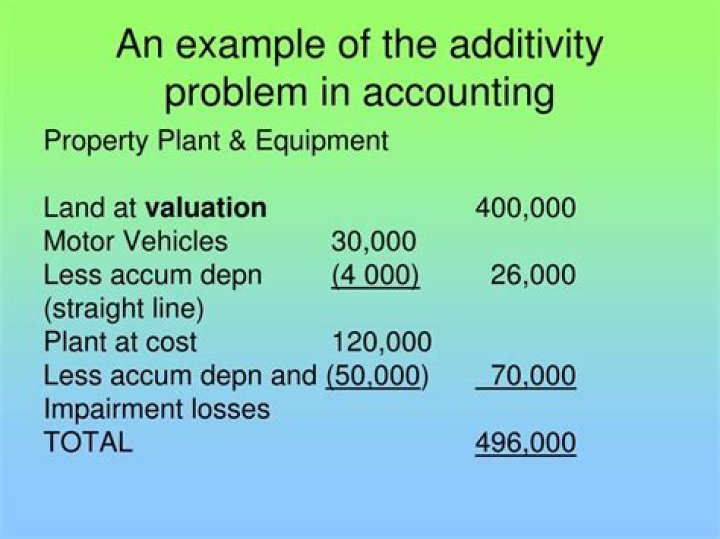

A mixed measurement model of accounting refers to an approach to accounting wherein a variety of measurement approaches are used to measure assets and liabilities. No one basis of measurement is prescribed for all classed of assets and liabilities.

Similarly, why is measurement important in accounting? Overview of Accounting and Measurement Accounting is the most important part to run a business as it gives a clear presentation of what is happening in the business. It is used to measure the economic posting and economic performance of the company. Its working measurement principle is fair value approach.

Thereof, what is measurement theory in accounting?

Accounting measurement is the computation of economic or financial activities in terms of money, hours, or other units. An accounting measurement is a unit of some measurable element that is used to compare and evaluate accounting data. Accounting is often measured in terms of money.

What are the measurement bases used in accounting?

Measurement is the process of determining the monetary amounts at which the elements of the financial statements are recognized and carried in the balance sheet and income statement. Usually four bases of measurement are used (1) Historical cost, (2) Current cost, (3) Realizable value, and (4) present value.

Related Question AnswersWhat is measurement uncertainty in accounting?

"Uncertainty" in accounting refers to the difficulty of predicting outcomes because of limited or inexact knowledge. Financial statements often contain estimates and other information based on uncontrollable events that can impact future financial reporting and transactions.What is mixed attribute measurement model?

Mixed attribute measurement model: It is a measurement basis to measure the value of assets and liabilities under “US GAAP (Generally Accepted Accounting Principles)” and “IFRS (International Financial Reporting Standards)”.Should be fair value a single measurement base in financial accounting?

In such a situation, a unique market value can be attributed to every asset and liability, so a single measurement method, consistent with fair value is appropriate. Such properties as consistency and comparability can then be achieved in a very precise sense.What is unit of measurement in accounting?

The unit of measure concept is a standard convention used in accounting, under which all transactions must be consistently recorded using the same currency. Without a common unit of measure, it would be impossible to produce financial statements.What are the basic principles of accounting?

Some of the most fundamental accounting principles include the following:- Accrual principle.

- Conservatism principle.

- Consistency principle.

- Cost principle.

- Economic entity principle.

- Full disclosure principle.

- Going concern principle.

- Matching principle.

How is relevance used in accounting?

Relevance is the concept that the information generated by an accounting system should impact the decision-making of someone perusing the information. This improves the speed with which various internal and external parties receive the financial statements, which improves the relevance of the information they receive.What is the measurement phase of accounting?

The measurement phase of accounting is accomplished by this. Stating assets and liabilities and changes in them in terms of a common financial denominator is a prerequisite in measuring financial position and periodic net income.What is recognition in accounting?

In accounting recognition is the act of including a transaction of a financial statement-either the income statement or the balance sheet.What is the most common basis of measurement used in financial statements?

Historical cost: Historical cost is the most common measurement basis adopted by enterprises in preparing their financial statements. This is usually combined with other measurement basis, such as current cost basis, realisable basis, etc., which are discussed later in this section.What is the cost principle in accounting?

Definition of Cost Principle The cost principle is one of the basic underlying guidelines in accounting. It is also known as the historical cost principle. The cost principle requires that assets be recorded at the cash amount (or the equivalent) at the time that an asset is acquired.How do you make an accounting presentation interesting?

Use these tips to make a financial presentation interesting and make sure people listen to what you have to say.- Communicate the story behind the data.

- Follow the 10-20-30 rule.

- Hide your notes and bullet points.

- Make it picture perfect.

- Channel the pros.

- Arrange for discussion.

- Open and close.