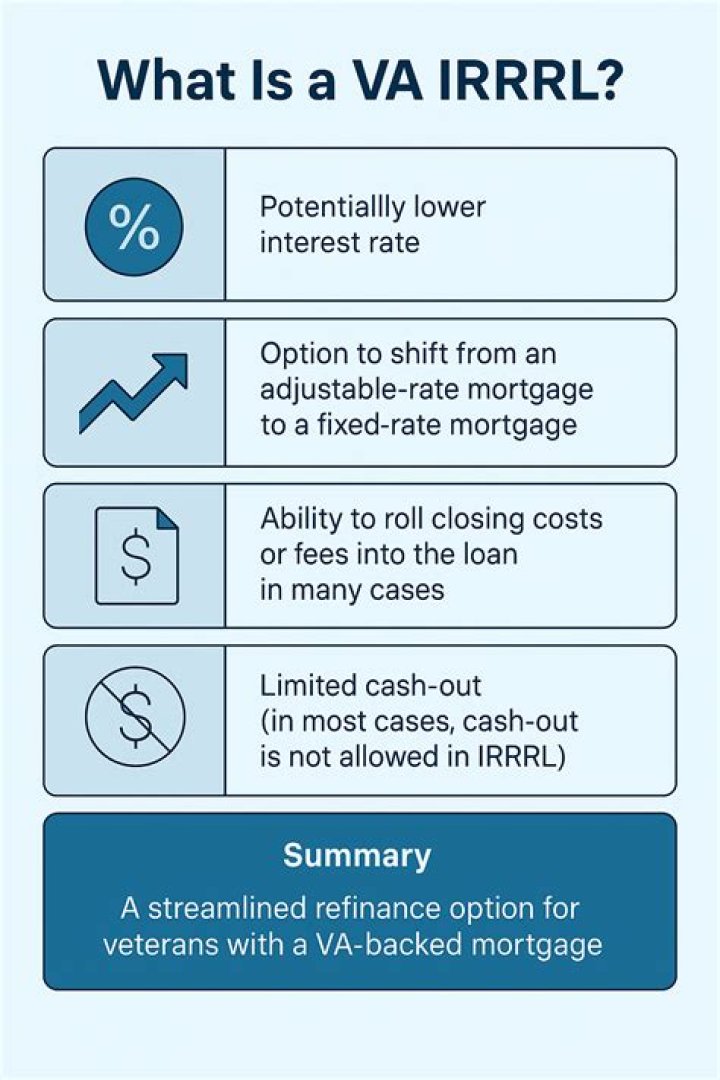

You are current on payments with no more than one 30–day late payment within the past year.Your new rate and monthly payment for the IRRRL must be lower than the previous loan’s monthly payment. … You must not receive any cash from the IRRRL.

What are the rules for a VA Irrrl?

- You are current on payments with no more than one 30–day late payment within the past year.

- Your new rate and monthly payment for the IRRRL must be lower than the previous loan’s monthly payment. …

- You must not receive any cash from the IRRRL.

What are the pros and cons of a VA Irrrl?

- Save money by lowering your interest rate.

- In most cases no appraisal is required.

- Employment proof is usually not needed.

- No dept to income verification.

- No minimum FICO score check.

- Change your loan terms.

- Faster closing times.

- Option to defer two months of mortgage payments.

Is the VA Irrrl program worth it?

A VA Streamline Refinance may not be worth it if you’ll pay more in closing costs than you’ll save. And it won’t help you cash out your home equity. If you want to refinance with cash back – to pay for home improvements, for example – you’ll need to use the VA cash–out refinance or another cash–out loan program.Does VA Irrrl have closing costs?

Closing Costs & Loan-to-Value (LTV) Unlike with a VA purchase loan, homeowners seeking an IRRRL can finance all of their closing costs, including up to two discount points and the VA Funding Fee. IRRRL borrowers who are not exempt will need to pay the VA Funding Fee.

Can you take cash out on a VA Irrrl?

You can’t take cash out of your home – Unlike the VA cash-out refinance, the IRRRL doesn’t allow you to receive any cash proceeds during the loan process. This is a major downside if you have a lot of home equity and you want to use it to pay down debt, pay for home improvements or reach another financial goal.

Can you shorten term on VA Irrrl?

The VA allows veterans to refinance into either the same length term, a shorter term, or a longer term. The only restrictions that apply to the loan term are if you plan to go longer. The VA only allows you to add up to 10 years onto the loan, but you cannot exceed 30 years and 32 days.

How much does a VA refinance cost?

VA refinance fees On a VA cash-out refinance, it’s 2.3% of the total loan unless it’s not your first VA loan. The funding fee is 3.6% on subsequent VA loans.Can I do a 15 year Irrrl?

Can I refinance a 30-year mortgage to a 15-year with an IRRRL? Refinancing to a 15-year mortgage is entirely possible and very common. The lifetime interest cost of a shorter loan will be less than a 30-year mortgage. However, the monthly payments on a 15-year mortgage can be significantly higher.

Can you do a VA Irrrl on an investment property?VA IRRRL requirements For a VA IRRRL, you only need to certify that you previously occupied the home (so the house can be an investment property, a rental property, or a second home). The interest rate on the new loan must be lower than the rate on the old loan unless you’re refinancing an ARM to a fixed rate mortgage.

Article first time published onIs a VA Irrrl a qualified mortgage?

On May 9, 2014, the Department of Veterans Affairs (VA) issued an interim final rule defining a qualified mortgage (QM) for VA insured and guaranteed loans. … Note that while all VA IRRRLs (also known as streamlined refinance loans) are considered QM loans, not all such IRRRLs are safe harbor QM loans.

How long do you have to be Irrrl?

How soon can you do a VA IRRRL? In 2018, the Protecting Veterans from Predatory Lending Act became law. It requires a seasoning period of either 210 days from the date of the first payment or after the sixth monthly payment (whichever’s longer) before an existing VA loan can be eligible for an IRRRL.

Can closing costs be rolled into a VA loan?

The VA loan allows you to include some of the closing costs into your total loan amount. The big thing is that you can roll your funding fee into the total mortgage amount. Although you’ll pay more in interest, this can help you get into a home now.

Do VA Irrrl require a pest inspection?

You still don’t need a pest inspection on a VA IRRRL refinance. But, you do need it on a standard VA refinance. This occurs when you take cash out of your VA loan or refinance from another loan type to a VA loan.

What is the maximum cash back on a VA Irrrl?

In the case of IRRRL/Streamline refinancing loans, borrowers are only permitted cash back under one circumstance if they are given a reimbursement for the cost of energy efficient improvements. This reimbursement can be up to $6,000, and the improvements must have been made within 90 days of closing.

How many times can I refinance my VA loan?

One of the most common questions from borrowers who have purchased a home with a VA loan is if they are able to use their benefit again. Fortunately, there is no limit on the number of times a Veteran can use the loan program. It’s a lifelong benefit for those who have served our country.

Is refinancing a VA loan a good idea?

When Is a VA Mortgage Refinance Worth It? … In general, lenders offer more favorable refinance rates to those with a steady income, a history of responsible credit use, and a low debt-to-income ratio. So if you have a strong credit profile and can secure low rates, this can be a worthwhile option for you.

Can you subordinate on a VA Irrrl?

The Department of Veterans Affairs official site reminds lenders that “No loan other than the existing VA loan may be paid from the proceeds of an IRRRL.” That means that home owners with a second mortgage must request that the lender of that second mortgage allow that mortgage to be a subordinate lien so that the VA …

What is the current VA funding fee for 2021?

2021 VA Funding Fees For Purchase And Construction Loans For cash-out or regular mortgage refinance, first-time borrowers will pay a 2.3% funding fee, while subsequent borrowers pay 3.6%.

What is the lowest VA Irrrl rate?

VA Loan TypeInterest RateAPR15-Year Fixed VA Purchase2.750%3.216%30-Year Streamline (IRRRL)3.125%3.272%15-Year Streamline (IRRRL)2.750%3.016%30-Year VA Cash-Out2.750%3.115%

How can I avoid closing costs with a VA loan?

Now, you know there are closing costs on VA loans, but what if you don’t want to or cannot bring those costs to closing? The most common way to overcome bringing these funds to closing is by seller paid closing costs and VA sales concessions. Remember, the seller is NOT required to pay the buyer’s closing costs.

What documentation is needed for a VA Irrrl?

You currently have a VA Loan. Certificate of Eligibility. Your existing VA loan is at least 6-months old. You have not been late on payments on your existing VA Loan in past 6 months OR if you’ve had it longer we can allow one 30 day late in past 12 months.

How often can I use VA Irrrl?

Overall, you can use the VA IRRRL program as often or as much as you want as long as there is a benefit. Eventually, you will get to the point that there is no point to the refinance. Instead, it will cost you more in closing costs and funding fees than it would benefit you to refinance your loan.

Why do sellers hate VA loans?

Many sellers – and their real estate agents – don’t like VA loans because they believe these mortgages make it harder to close or more expensive for the seller. … Are less likely to close than other types of mortgages. Take ages to reach closing.

Do you pay PMI on a VA loan?

VA loans also don’t require private mortgage insurance (PMI), but you will pay a VA funding fee when you close, which will be a percentage of the loan’s total value. That fee helps keep the program running for future borrowers.

Who pays for a VA appraisal?

The lender hires the appraiser, but generally the buyer pays for the appraisal. VA appraisal costs vary by region. In the Northwest, fees might run $800 or more, while in the Midwest and the South, the cost might be closer to $450.

Can a Veteran pay for repairs on a VA loan?

The reality is VA buyers can pay for home repairs needed to close a loan, even if they’re issues related to the VA’s Minimum Property Requirements. … To be sure, if the VA appraisal indicates there are repairs needed, buyers should first ask the seller to cover these costs.

Should I sell my house to someone with a VA loan?

Using a VA loan means you’ll end up saving money both on the purchase and over the life of the loan. However, it does mean the person selling you the house will have to spend more to sell you the house. If you’re worried about the seller denying your offer because you’re using a VA loan, don’t be.

What will fail a VA inspection?

During the inspection, they’ll check for any wear and tear or issues that could cause the system to fail shortly after the sale goes through. If they determine that the system isn’t able to heat the house to at least 50 degrees Fahrenheit during the winter without issue, the house will fail the inspection.